August 2024 / MARKETS & ECONOMY

U.S. election and trade policy: What investors need to know

Presidential election will shape the pace of deglobalization.

Key Insights

- Deglobalization, support for U.S. industry, and competition with China—these touchstones are likely to inform trade policy no matter who wins the election.

- Trump would likely focus on trade deficits and use trade as a negotiating tool. Harris would likely favor a multilateral approach to competing with China.

- For investors, understanding companies’ exposure to overseas supply chains and their potential to increase prices in response to rising costs will be critical.

Deglobalization, support for key domestic industries, and economic competition with China—these touchstones are likely to inform U.S. trade policy whether Democrat Kamala Harris or Republican Donald Trump wins the election.

But how each of the major-party presidential candidates would seek to make free trade fairer from the perspective of U.S. interests differs dramatically in scope and approach.

These divergences could have important implications for markets, industries, and geopolitics during the next president’s time in office and beyond.

A Trump presidency would likely focus on trade deficits

Former President Trump and some of his key advisers have tended to regard significant trade deficits with other countries as potential signs of unfair competition and a detriment to the U.S. economy.

During Trump’s four years in the White House, his administration sought to alleviate some of these imbalances by imposing tariffs on roughly USD 380 billion worth of imports, the bulk of which were from China.

In the runup to the 2024 election, Trump repeatedly has floated a 10% border tax on all goods coming to the U.S. from abroad and a tariff as high as 60% on imports from China.

Setting aside feasibility and the specific numbers, these pronouncements signal that a second Trump administration likely would take an aggressive stance on trade policy that would extend beyond China.

Such an approach could set the stage for extracting concessions, either on trade or to further other policy objectives.

Trade restrictions focused on specific industries or companies could also be in the cards, along with efforts to institute stronger rules on goods’ country of origin.

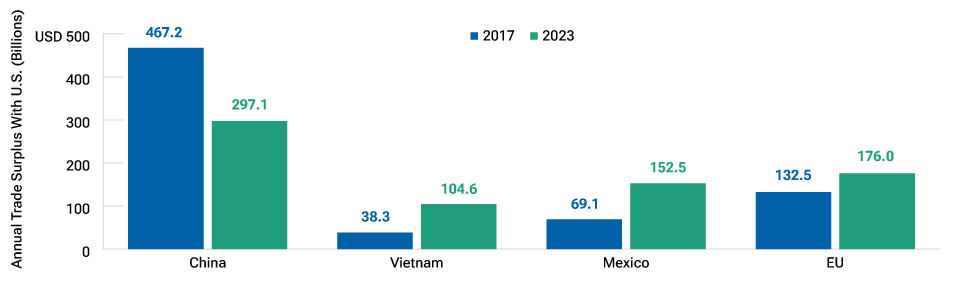

Companies seeking to avoid tariffs have taken to shipping their products from or assembling them in countries with which the U.S. has free trade agreements. This workaround appears to be one of the reasons that U.S. trade deficits with countries such as Vietnam and Mexico have increased as its trade imbalance with China has declined somewhat (Figure 1).

U.S. trade deficit has shrunk with China and expanded with Mexico and Vietnam

(Fig. 1) Annual trade surplus with the U.S., 2017 and 2023

As of February 7, 2024

Source: U.S. Census Bureau via FactSet.

How personnel can shape policy

Broad strokes aside, the specifics of Trump’s trade policy are difficult to predict—as are the possible responses of the affected countries.

If Trump wins the election, I’ll be paying close attention to the views of key appointees, especially the U.S. trade representative and the secretary of the Treasury. Who Trump puts in charge of specific agencies will shape the debate within the administration and drive policy outcomes.

Less is known about Harris’s views on trade. However, if she were to win the presidency, her administration would likely retain a good deal of personnel from the Biden White House, suggesting that certain themes could also carry over to how it might handle trade.

A Harris presidency would likely take its cues from Biden’s trade policies

What characterized the Biden-Harris administration’s approach to trade? Much of the emphasis has been on economic competition with China.

During his presidential term, Joe Biden left in place the tariffs that Trump levied on Chinese imports. His administration also took targeted actions on trade that tended to be informed by national security considerations and efforts to strengthen domestic industry:

- Semiconductors and artificial intelligence (AI): Via export controls and rules on outbound investment, Biden sought to limit China’s access to the tools and expertise needed to produce the advanced chips and other technologies at the heart of AI and quantum computing.

- Protecting against overcapacity: The Biden administration recently introduced tariffs affecting a modest USD 18 billion worth of goods imported from China. These measures focused on industries where China has squeezed competition by building up excess productive capacity, including electric vehicles, steel and aluminum, and solar power components.

In addition to focusing on strategically important industries, a Harris administration would probably favor a multilateral approach to trade policy, seeking to engage traditional U.S. allies.

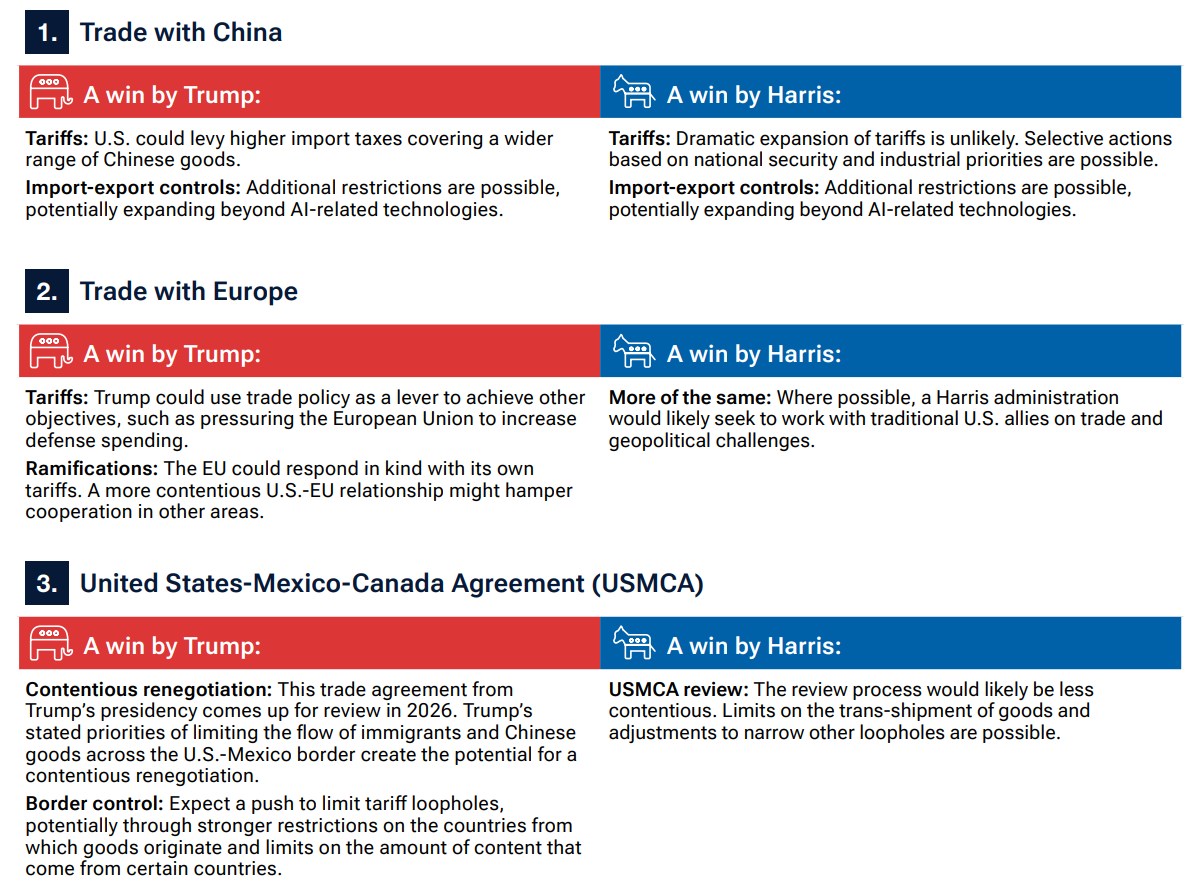

Three areas where the election outcome could make a difference:

U.S. election could shape the pace of deglobalization

Protectionist impulses should remain alive and well in Washington, regardless of which party is in the White House.

A Harris presidency would likely take a measured approach to trade policy that focuses on competition with China. Trump has signaled that he favors a more aggressive tack that would accelerate the process of deglobalization.

Amid these uncertainties, deep fundamental research can be a critical differentiator. The investment professionals at a well-resourced global asset management firm, for example, may be better positioned to understand individual companies’ exposure to overseas supply chains and their potential to increase prices in response to rising costs.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.

Gilad Fortgang is an associate analyst covering Washington and regulatory research in the T. Rowe Price Investment Management U.S. Equity Division.