July 2024 / FIXED INCOME

Ahead of the Curve - “Shadow banking system” creates a trickier path for the Fed

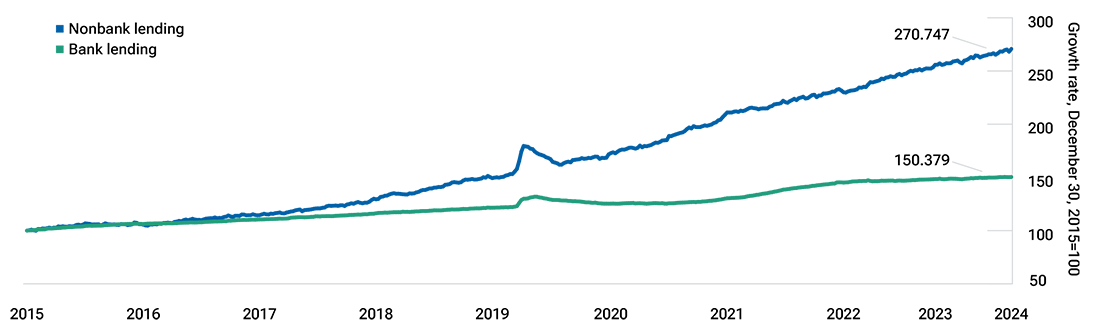

Rise in nonbank lending drives banks to shift risk exposure

During our fixed income policy week discussions, participants examine dozens of charts that our portfolio managers, analysts, and economists present on an array of market topics. One that particularly stood out for me recently showed the rapid growth of nonbank lending in the U.S. over the last eight years and what that could mean for investors. While traditional bank lending has also increased, the rate of credit creation by nondepository institutions in the “shadow banking system” easily outpaced it. Coincidentally, I have received a number of questions on this topic as I have traveled to meet clients recently.

This trend has received considerable attention in the financial media, but I wondered what it means for the banking system in the long run. I consulted credit analyst Pranay Subedi, who co‑covers U.S. banks and finance companies and has devoted much time and energy analyzing the interaction between the Federal Reserve’s monetary policy stance and the banking system. Here is a summary of our discussion.

What are the factors driving growth in nonbank lending?

Since the global financial crisis, an increasing share of credit is created by nonbank lenders such as mortgage originators and private credit funds. This is a well‑documented trend largely stemming from a combination of increased bank regulation and a greater ability of nonbanks to underwrite credit due to technological improvements and a larger capital base.

While the common narrative is that banks are being disintermediated, the reality is that the role of banks within the economy is changing.

Can you provide a quick primer on how banks create economic value?

As banks adapt their business models, the very nature of how they create value is also changing.

Setting aside fee income and capital markets activity, core bank value creation takes place through both sides of their balance sheets:

- Asset side: Banks extend loans to borrowers, adding value by monitoring borrowers and processing nonpublic information.

- Liability side: Banks pay below‑market rates for funding in the form of deposits, adding value by offering depositors access to a “safe” store of value and to the payments system.

The two channels interact with each other—for instance, by allowing banks to finance long‑term illiquid loans using demandable deposits that they believe are not prone to runs.

These sources of value creation require banks to take a combination of interest rate, liquidity, and credit risk. The growth of nonbank lending has led to banks creating less value on the asset side and less credit risk on the balance sheet of banks.

Nonbank lending has skyrocketed

(Fig. 1) Growth in nonbank and bank lending since 2016.

As of June 5, 2024

Source: Bloomberg Finance L.P.

How has the balance of risks for banks evolved?

Many banks are responding to these changes by taking on more liquidity risk. This shift is an important transition for bondholders.

Despite credit risk leaving the banking system, deposit growth has been rapid in the U.S., with deposits as a percentage of gross domestic product (GDP) rising from the mid‑30% area in the 1990s to over 60% today.1 Importantly, larger, uninsured deposits have increased over this time. Deposits are created through two main channels:

- Credit growth

- Bank loans as a percentage of GDP have climbed from 30% to 44%1 since the 1990s. Loans create deposits.

- Quantitative easing (QE)

- The Fed significantly expanded its balance sheet through multiple rounds of QE, which creates bank reserves and can create deposits under certain conditions.

In the case of QE, banks, now flush with reserves, issue short‑dated liabilities by accepting uninsured deposits. This allows them to match the maturity of their assets and liabilities, minimizing interest rate risk.

At the same time, QE leaves banks significantly more liquid than before. After all, their less liquid bonds have been swapped for highly liquid bank reserves. Ideally, banks would take advantage of this liquidity to underwrite credit, but as discussed earlier, bank regulation and growing nonbank lending limit their ability to do so.

Instead, banks take advantage of their liquidity position by making commitments to supply liquidity, such as revolving credit facilities. When I study these facilities, I find they tend to be senior and secured, and have little credit risk. As an aside, these facilities are often extended to the same parties that banks are losing loan share to, including mortgage originators and private credit funds.

While these facilities have minimal credit risk, they generate liquidity risk for the bank. When the Fed is undertaking QE and the banking system is flush with liquidity, banks increase the volume of lines they are writing. However, when the Fed starts quantitative tightening (QT), the banking system might not pull back on these lines quickly enough. As QT progresses, it will eventually start draining liquidity from the banking system, removing the liquid resources that banks are using to write revolving credit facilities against.

The risk banks are taking is that their uninsured deposits may leave while the revolving credit facilities are drawn—all while QT makes them less liquid.

How could the interaction of QT and the movement of credit outside the banking system play out?

This will likely first lead to higher pricing on the revolving credit facilities and then eventually to slower growth in these facilities. Alternative sources of funding such as collateralized loan obligations (CLOs) and life insurance companies could act as an offset to some extent, but they will not be able to provide financing as flexibly or at prices as attractive as banks.

As is usually the case with liquidity risk, a removal of bank reserves beyond the banking system’s lowest comfortable level of reserves (LCLoR) could cause disruptions in short‑term funding markets—as it did in 2019.

How would authorities respond to stress in the nonbank financial system?

During periods of market stress, we often see heightened demands for liquidity. In the case of nonbank financials, liquidity demands could stem from a margin call for a levered investor, a direct lender that wishes to support one of its own portfolio companies, or a private credit vehicle that spots an investment opportunity. These nonbank lenders would turn to banks to meet these liquidity requirements—at the exact same time that banks themselves may be dealing with a shortage of liquidity, perhaps from elevated deposit flight.

Liquidity dependence in the financial system means that the Fed’s response would involve pushing new liquidity into the financial system, either directly to banks through new reserves, or to nonbank participants such as money market funds or corporate bond markets (as was the case following the onset of the coronavirus pandemic). These responses have been highly effective at calming liquidity stress in the past. While stress may begin outside the banking system, the regulatory response will very likely run through the banking system.

The link between rising nonbank lending and the Fed

The Fed wants to avoid having the banking system’s reserves fall below the LCLoR and would probably need to end QT to circumvent the situation (or shorten it if it occurs). This link between the rise of nonbank lending, the banking system, and QT is one important reason why I believe an earlier‑than‑expected end to QT is likely. This insight also presents an excellent example of how our global credit research platform can go beyond the well‑publicized market trends to examine their longer‑term implications.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.

Arif Husain is the head of Global Fixed Income and chief investment officer of the Fixed Income Division. He is chairman of the Fixed Income Steering Committee and a member of the firm’s Management Committee. Arif is lead portfolio manager for the Global Government Bond High Quality Strategy. He is a vice president of T. Rowe Price Group, Inc., and T. Rowe Price International Ltd.