June 2024 / MULTI-ASSET INSIGHTS

Navigating the model portfolio landscape

Key considerations for model selection and implementation.

Key Insights

- Model portfolios present financial professionals with opportunities to save time, streamline the investment process, and improve client outcomes.

- We believe model portfolios should be evaluated on six key factors: experience, strategic portfolio design, tactical asset allocation, underlying components, due diligence, and ongoing support.

- A well-defined process for model selection and a clear view of what factors matter most can help financial professionals in their model searches.

The popularity of model investment portfolios[1] has surged in recent years, as have the number and variety of offerings available. Model portfolios allow financial professionals to streamline their investment process, potentially improve risk/return outcomes, and—most importantly—increase time spent with their clients. However, as the model portfolio industry evolves, financial professionals must weigh a range of considerations in order to select model portfolios on behalf of their clients.

A complex landscape

Since Morningstar launched its model portfolio database in 2019, over 2,700 U.S. models have been reported. Some of the largest providers offer more than 75 individual portfolios.[2]

Broad peer groups may complicate model selection

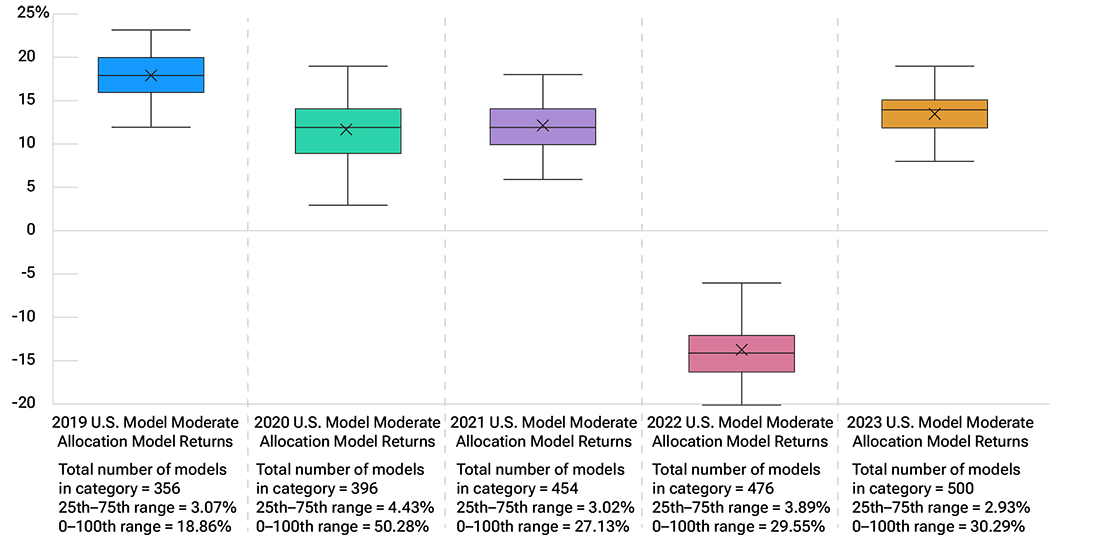

(Fig. 1) Return dispersion for U.S. models in Morningstar’s U.S. model moderate allocation category

As of December 31, 2023.

Past results are not a reliable indicator of future results.

Source: Morningstar Direct (see Additional Disclosures). All data analysis by T. Rowe Price. The cross (“x”) is the mean annual return, the center horizontal

line is the median annual return. The box represents the middle 50% of all the annual returns. The upper and lower whiskers are the maximum and

minimum annual returns per model over the period studied that are within 1.5 times the middle 50% of all the annual returns.

A broad range of returns

Evaluating model portfolio performance presents a unique challenge. In this evolving space, Morningstar’s peer groups remain broadly defined, and, for model portfolios that do have reported returns, absolute and relative performance within those peer groups can be highly variable.

We examined the investment performance reported in Morningstar’s U.S. Model Moderate Allocation category to better understand the range of returns for model portfolios within the peer universe. We found that the return dispersion[3] within the category was 31%, on average, over the past five years and widened as more models launched (Figure 1).[4]

Our analysis suggests that such dispersion can be attributed to a variety of factors, including:

- portfolio construction choices

- the level of diversification or concentration within a model portfolio

- the split between active and passive management within models

- the underlying component security selection and tracking error[5]

- whether a model is more strategic or tactical in nature

As the model landscape continues to evolve and the regulatory environment shifts, we believe financial professionals need to have a well‑defined process for model selection and ongoing monitoring.

Considerations for model selection

In a fast‑growing space with many options and highly variable outcomes, comprehensive due diligence can be a daunting task. We believe there are a few key considerations that can help financial professionals identify appropriate options for their clients.

Model portfolios are not created equal

(Fig. 2) Evaluating the differences between models can help financial professionals navigate a complex landscape.

An Experienced Provider |

— Who manages the portfolio, and what’s their track record for delivering asset allocation guidance? — What is the portfolio manager’s reputation, and what qualities are associated with its culture? — Do these qualities align with your own perspective and your clients’ goals? |

Strategic Portfolio Design |

— How did the portfolio manager arrive at a particular asset mix or global diversification profile? — Is the portfolio’s target mix of asset classes consistent with your individual client’s objectives, risk tolerance, and time horizon? |

Tactical Asset Allocation |

— Is tactical asset allocation a feature of the model? — Does the manager have a track record of improving outcomes through tactical asset allocation? — How frequently and at what magnitude are the model portfolios rebalanced? |

Underlying Components |

— How were the underlying components selected? Are they entirely proprietary, or are third-party funds included? — Are the underlying funds actively or passively managed, or do they include a mix of both? How was this distribution determined? — What is your individual client’s fee budget and cost sensitivity? Is there an overlay fee, or is the fee a weighted average of underlying funds? |

Due Diligence |

— What processes does the manager have in place to monitor and manage the portfolio’s underlying strategies and or potential risk exposures? — If the model includes non-proprietary strategies, how does the manager select, size, evaluate, and as needed replace these exposures? |

Ongoing Support |

— What kind of support does the model provider offer to help keep you and your clients informed about their model portfolios and overall market conditions? |

An Experienced Provider: It’s worth asking who manages the portfolios as not all models have dedicated portfolio management teams. It can be helpful to examine the manager’s track record for delivering asset allocation guidance. Moreover, what is the portfolio manager’s reputation, and what qualities are associated with the firm’s culture? These qualities should align with the financial professional’s own perspective and their individual clients’ goals.

Strategic Portfolio Design: Starting from a broad universe of options, financial professionals typically narrow the search by identifying portfolios appropriate for a client’s investment goals and risk tolerance. Some model portfolios are designed to target particular outcomes, such as capital appreciation or income generation, while others may be intended to fill in gaps in existing portfolios. Portfolio design is a critical consideration in the selection process. How did the portfolio manager arrive at a particular asset mix or global diversification profile? The strategic allocation determines the target mix of different asset classes over the long term and should be consistent with an investor’s objectives, risk tolerance, and time horizon.

Tactical Asset Allocation: A model portfolio’s approach to tactical asset allocation is another important consideration. Some model portfolios may feature tactical asset allocation guidance—incremental or significant moves to overweight or underweight certain asset classes based on shorter‑term market views, with the goal of enhancing returns or mitigating risks. If tactical allocation is a feature of the model, we believe financial professionals should consider how these tactical views are implemented in the portfolio, as well as their frequency and magnitude. Tactical asset allocation can potentially enhance the value proposition of a model portfolio as the manager can dynamically shift positioning based on forward‑looking views, but more meaningful deviations in the long-term asset or sub-asset class levels may shift the portfolio away from the client’s objectives or from its intended role in the client’s broader allocation. Further, meaningful turnover generated from tactical positioning may create additional considerations for tax consequences. Does the manager have a track record of improving outcomes through tactical asset allocation? Additionally, how frequently are their model portfolios rebalanced?

Underlying Components: In addition to considering the overall design and management of the model at the top level, we believe financial professionals should examine the characteristics of the model’s underlying components and look for models that feature underlying investment vehicles that also have experienced management teams with track records of delivering strong absolute and relative performance over full market cycles. Some of the questions we believe financial professionals should ask:

- How were the underlying components selected? Are they entirely proprietary, or are third‑party funds included?

- Does the model use mutual funds and/or exchange‑traded funds?

- Are the underlying funds actively or passively managed, or do they include a mix of both? How was this distribution determined?

- What are the historical and forward‑looking tracking errors of the underlying funds?

- Were the funds selected with an awareness of tax implications?

- What is your client’s fee budget and cost sensitivity? Is there an overlay fee, or is the fee a weighted average of underlying funds?

Due Diligence: It is important to consider risk management and the ongoing oversight of the overall model portfolio and the underlying components. For instance, what processes are in place to monitor and manage the portfolio’s underlying strategies and or potential risk exposures? How often do the model portfolio managers meet with the underlying strategy teams? Who is responsible for monitoring adherence of underlying strategies to their stated objective and investment processes? How are underlying strategies monitored (e.g., process, philosophy, people, and performance)?

Ongoing Support: Finding a model portfolio that meets client needs can be a daunting task. We believe a final consideration for financial professionals is the quality of ongoing support they receive from the model portfolio provider. What kind of support (e.g., marketing or distribution) does the model provider offer to help you and your clients stay informed about the model portfolios and overall market conditions? In our view, this support plays an important role as financial professionals seek to build their practice and can help educate clients on portfolio performance, positioning changes if the model includes tactical shifts, important market themes, and the rationale behind the investment decisions reflected in a model.

Ways to implement model portfolios

The below illustrations show potential model approaches, and is not an all‑inclusive list. The asset classes/sub‑asset classes noted are also for illustrative purposes only. This material is not intended to be investment advice or a recommendation to take any particular investment action. The opinions and commentary provided do not take into account the investment objectives or financial situation of any particular investor or class of investor. Please consider your own circumstances before making an investment decision. All investments are subject to market risk, including the possible loss of principal. Diversification cannot assure a profit or protect against loss in a declining market. There is no assurance that any investment objective will be achieved.

A variety of approaches

Just as models may be highly varied in their portfolio construction and design, financial professionals can use models to address a wide range of client needs and in a variety of ways. For some clients, allocating to a single model might be an appropriate approach, while other clients may benefit from using models to augment their existing portfolios, or even a combination of multiple models to achieve a diversified allocation. The five possible illustrative approaches above demonstrate potential benefits and some considerations that we believe financial professionals may want to examine for each approach.

Conclusions

The model landscape continues to evolve and offers a wide range of options from outcome‑oriented to target allocation to completion portfolios. In a subsequent study, we detail T. Rowe Price’s approach to model portfolio design and management.

Model portfolios offer access to institutional‑quality expertise, scalable and diversified investment solutions, and ongoing support to deliver insights, services, and solutions to financial professionals and their clients.

However, the potential benefits of using model portfolios are rivaled by the challenges in identifying options for clients in an increasingly complex space. We believe a well‑defined process for model selection and a clear view of what factors matter most can help financial professionals in this process.

A hypothetical all‑in‑one model approach

(Fig. 3)

Role |

Offers an efficient way to access diversified model portfolios that seek to meet a variety of client goals and risk objectives. |

Potential Benefits |

A fully outsourced investment management process, including strategic asset allocation, fund selection, tactical asset allocation (if applicable), and risk monitoring. |

Potential Considerations |

Investment professionals may be more reliant on content provided by the model manager to keep themselves and their clients abreast of model changes andtheir rationales. |

Source: T. Rowe Price. For illustrative purposes only.Not representative of an actual investment.

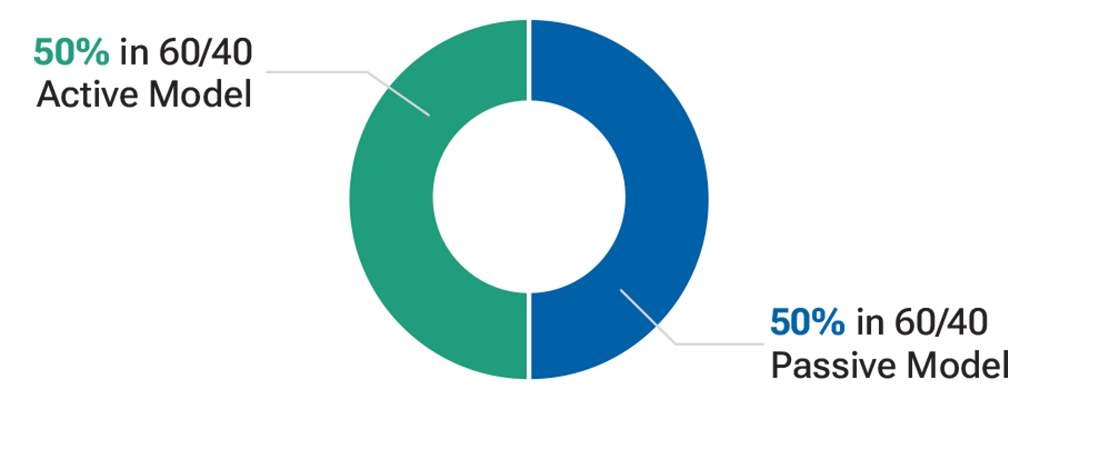

A hypothetical multi‑model active/passive approach

(Fig. 4)

Role |

A “model of models” combining an active and a passive diversified model with similar asset allocations. |

Potential Benefits |

Potentially offers more flexibility for investment professionals to combine models and control tracking error or cost consistent with their clients’ preferences and goals. |

Potential Considerations |

A single model that is explicitly active/passive in nature may be a more efficient approach as the management team may have considered which exposures to implement actively or passively. |

Source: T. Rowe Price. For illustrative purposes only.Not representative of an actual investment.

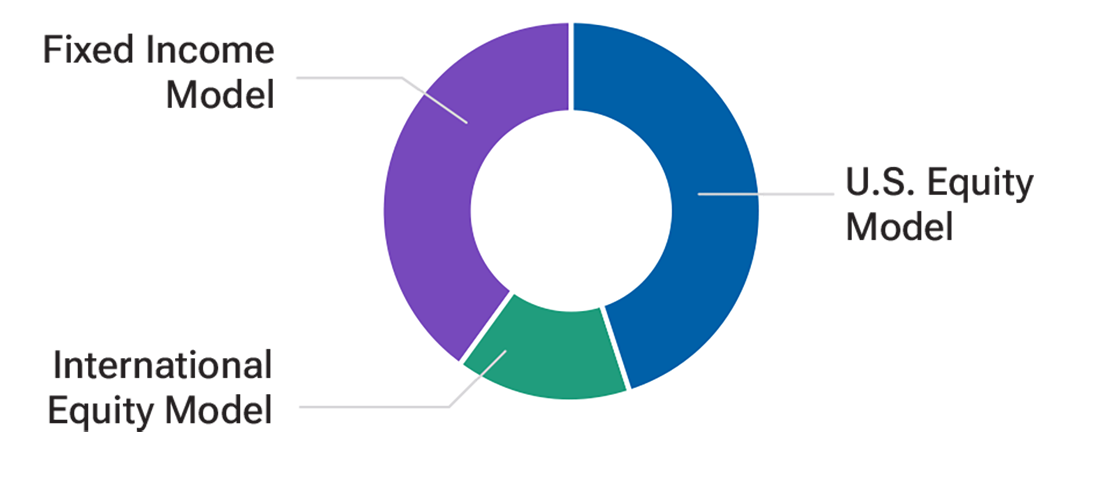

A hypothetical multi‑model building block approach

(Fig. 5)

Role |

A model selected by asset class or other building blocks from more than one model provider. |

Potential Benefits |

May offer increased customization opportunities; potentially may provide efficient tactical levers (e.g., stocks versus bonds or U.S. versus non‑U.S. markets). |

Potential Considerations |

Strategic asset allocation is owned by the financial professional. Asset class exposure choices can have significant influence on absolute and relative performance. |

Source: T. Rowe Price. For illustrative purposes only.Not representative of an actual investment.

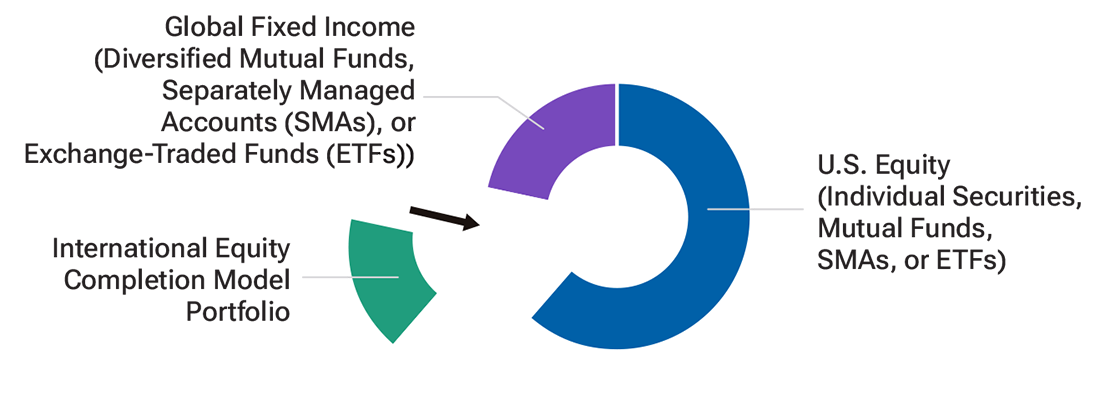

A hypothetical completion approach

(Fig. 6)

Role |

Fill in (i.e., complete) a client’s portfolio with a focused model portfolio to complement existing investment strategies. |

Potential Benefits |

For investment professionals who prefer to maintain portfolio management responsibility in an asset class, a completion approach offers a way to close gaps and potentially achieve efficient diversification. |

Potential Considerations |

There may still be gaps versus global markets. While a completion model can help close a portfolio gap, financial professionals should consider the level of diversification within the individual model investments and the resulting overall portfolio. |

Source: T. Rowe Price. For illustrative purposes only.Not representative of an actual investment.

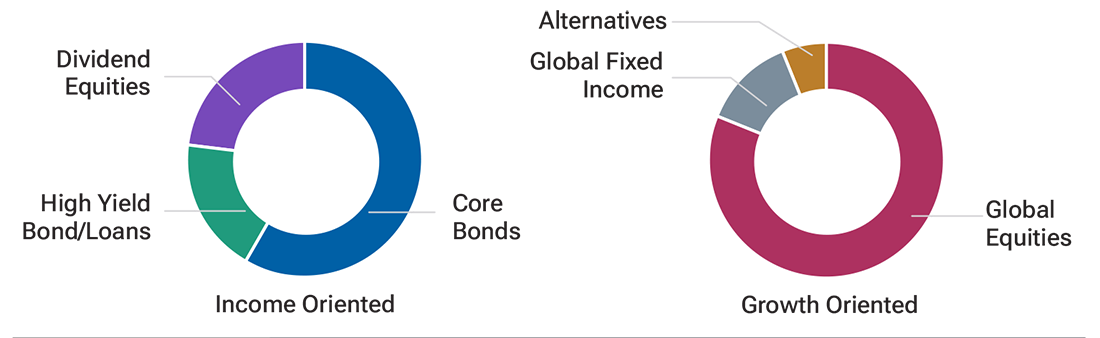

Hypothetical outcome‑oriented approaches

(Fig. 7)

Role |

Model portfolios that target a specified investment objective. |

Potential Benefits |

Potentially may map efficiently to specific objectives in ways that resonate with clients. |

Potential Considerations |

Be sure to look under the hood. Exposures may vary significantly across models with identically stated outcome objectives. For example, income-oriented models may reach for yield with relatively riskier asset classes. |

Source: T. Rowe Price. For illustrative purposes only.Not representative of an actual investment.

Important Information

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date written and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

Canada—Issued in Canada by T. Rowe Price (Canada), Inc. T. Rowe Price (Canada), Inc.’s investment management services are only available to Accredited Investors as defined under National Instrument 45-106. T. Rowe Price (Canada), Inc. enters into written delegation agreements with affiliates to provide investment management services.

© 2024 T. Rowe Price. All Rights Reserved. T. ROWE PRICE, INVEST WITH CONFIDENCE, and the Bighorn Sheep design are, collectively and/or apart, trademarks of T. Rowe Price Group, Inc.

Erin Garrett is a portfolio manager in the T. Rowe Price ActivePlus Portfolios Program, Target Allocation Active Series and an associate portfolio manager for the Target Allocation strategies. Erin is a vice president of T. Rowe Price Group, Inc., and T. Rowe Price Associates, Inc.

Christine Johnson is a vice president of T. Rowe Price Group, Inc., and the asset class product manager for the Multi-Asset and Alternative Strategies. Her focus is working with Research, Investments, and Distribution on product strategy, development, and management across the firm's global multi-asset product suite. Christine has over 25 years of industry experience. Prior to joining the firm in 2018, Christine was a managing director and head of Alternatives and Multi-Asset Product Management at AllianceBernstein. Prior to joining AllianceBernstein in 2013, she was a director at Deutsche Asset & Wealth Management, where she was responsible for alternative strategy and platform development. Before that, she was an investment specialist for alternative and asset allocation strategies, including hedge funds, real estate, and multi-asset strategies. Prior to Deutsche, she was an investment consultant at Bankers Trust Company, where she assisted plan sponsors with investment policy development, asset allocation, and manager selection. Christine earned a B.A. in finance, with a minor in economics, from Pace University and an M.B.A., with a double concentration in international finance and information systems, from Fordham University. She also has earned the Chartered Financial Analyst designation.

Christina Kellar is a multi-asset solutions strategist in the Multi-Asset Division. She is a vice president of T. Rowe Price Group, Inc., and T. Rowe Price Associates, Inc.