July 2024 / POLICY INSIGHTS

Are US smaller companies set to shine? Identifying the catalysts for a positive rerating

Attractive valuations aside, ultimately, a catalyst is needed to drive a positive rerating of U.S. smaller companies

Key Insights

- The current market cycle, which has been led almost entirely by large‑cap stocks, is looking increasingly long in the tooth.

- We are seeing early signs of investors moving out of richly priced, larger U.S. company names and into those offering better relative value down the market cap scale.

- Attractive valuations alone, however, are not enough. In this paper, we consider potential catalysts that could drive a positive rerating of U.S. smaller companies.

A new cycle of outperformance?

A great deal of ink has been dedicated to explaining how, for more than a decade, the performance of the U.S. equity market has been dominated by a small group of mega‑cap, growth‑oriented companies. This trend has seen the U.S. equity market become highly concentrated at the top end, with valuations of a small group of large companies increasingly hard to justify. Importantly, history tells us that as high concentration in the S&P 500 Index begins to unwind, a new cycle of small‑cap outperformance usually begins. Over the past century, large‑cap stocks and small‑cap stocks have alternated market leadership on a roughly 10‑year cycle.

As we stand today, the current market cycle, which has been led almost entirely by large‑cap stocks, is looking fairly long in the tooth. And investors, conscious of the need to diversify their portfolios, are looking for alternatives. As money is reallocated out of highly concentrated, potentially valuation‑stretched larger company names, it must find somewhere to go, and we are beginning to see this reallocation of funds down the market capitalization scale into relatively more attractively valued mid‑ and small‑cap stocks.

What’s more, it shouldn’t take a huge amount of capital flowing into the small‑cap domain to move the dial significantly. As of March 31, 2024, the five largest stocks in the S&P 500 Index had a market capitalization of some 3.7 times that of the entire Russell 2000 Index universe.1 So, every incremental dollar reallocated into the small‑cap sector is a tailwind to relative performance. If even a fraction of the value of the five largest U.S. stocks is reallocated into smaller companies, the overall impact could be substantial.

Potential catalysts to drive smaller companies higher

Of course, attractive valuation alone is not enough—U.S. smaller‑company valuations have been below their long‑term average for some time. Ultimately, the key question for investors is: What is the catalyst that could cause U.S. smaller companies to be rerated higher? And the simple answer here is earnings growth—higher earnings mean investors will be more willing to pay higher prices. And the outlook here is positive, with favorable structural trends providing support.

U.S. capital spending has accelerated post‑pandemic, and smaller‑company earnings are more highly correlated to capex growth than larger companies due to the largely domestic focus of these businesses. Spending on infrastructure, at the local, state, and federal levels, began to accelerate in 2021 in the aftermath of the coronavirus pandemic.

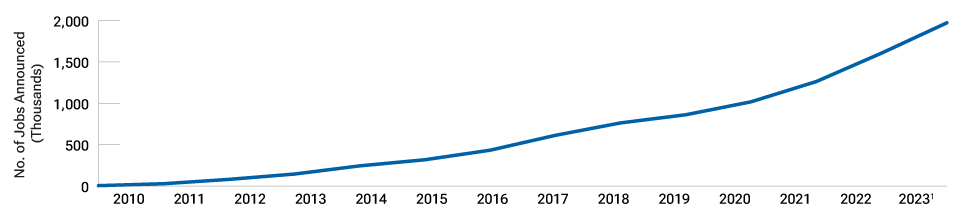

The reshoring/onshoring of U.S. business operations, particularly of manufacturing capacity, is another important secular trend that is highly supportive of smaller companies. The federal government has prioritized U.S. supply chain security in the wake of the pandemic‑era breakdowns, providing massive incentives to domestic businesses, enshrined in legislation such as the CHIPS and Science Act of 2022. Dollars from these programs are just beginning to flow in 2024, but individual companies began their investments in new U.S. manufacturing capacity even earlier. These investments represent long‑term support to the domestic economy and stand to benefit a wide range of companies, from construction and materials companies to those that provide the sophisticated automated assembly line components to the distributors and transportation companies critical to moving goods through the supply chain. The Economic Policy Institute also estimates that every manufacturing job that returns to the U.S. generates seven new jobs in supporting industries2—everything from more regional banks for lending, more housing for workers, and more restaurants to serve them (Fig. 1).

U.S. reshoring/onshoring is a huge boost for the domestic economy

(Fig. 1) Cumulative U.S. jobs announcements directly linked to reshoring

As of June 30, 2023.

1 Indicates full‑year projection based on first‑half 2023 data. Actual outcomes may differ materially from projections.

Source: Reshoring Initiative.

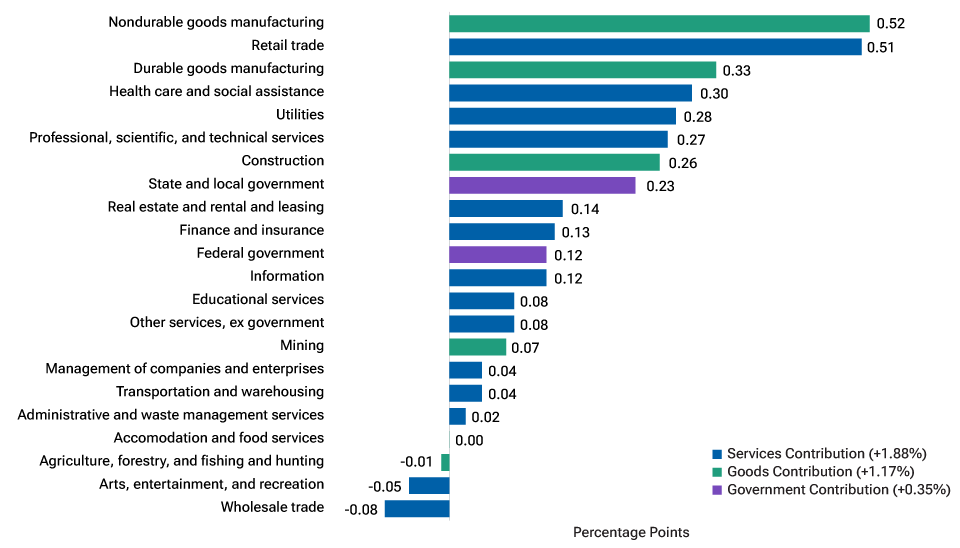

Given their more domestic orientation, smaller companies are more acutely positioned to benefit from shifting trends in the U.S. economy. One of the trends we are seeing is the shift in consumer spending from goods to services (Fig. 2). Bank of America Securities estimates that over 70% of the revenues of the Russell 2000 are derived from services, with less than 30% from goods. In contrast, the revenues of the S&P 500 are roughly 50–50.3 During the coronavirus pandemic, the goods economy remained relatively healthy, while the services economy all but shut down completely. This scenario is progressively reversing and, with smaller‑company earnings much more geared to the services sector, this should provide a significant boost to earnings growth broadly.

A resurgent U.S. services economy bodes well for smaller companies

(Fig. 2) Contributions to percentage change in real U.S. GDP by industry group, Q4 2023

Seasonally adjusted data, as of December 31, 2023.

Real U.S. GDP increased by 3.4% in Q4 2023.

Sources: Bureau of Economic Analysis and U.S. Department of Commerce.

An inflection in smaller‑company fundamentals?

Given these potentially significant structural tailwinds, we anticipate an inflection in smaller‑company fundamentals, as industries like real estate, the energy complex, and certain parts of the technology sector notably improve relative to the recent past. Improvement in these areas alone will support many small‑ and mid‑cap businesses and, in aggregate, boost earnings on a relative basis versus large‑cap peers. Within the three sectors mentioned, there are potentially rich stock‑specific opportunities to be found, as outlined below.

Technology is not all about AI: While some semiconductor companies are clearly benefiting from the rise of artificial intelligence (AI), other areas of technology are experiencing a sizable downturn in demand, having surged during the pandemic. However, the ever‑increasing technology demands—for complexity, performance, power management, and more—create long‑term opportunities. For smaller companies, perhaps the best opportunities could come from the second‑order effects of AI. For example, we are already seeing the rapid adoption of new AI apps that can learn and provide better outcomes for users. In turn, we see this driving renewed growth in mobile handsets, and we are spending a lot of time digging into these potential areas of indirect growth.

Real estate opportunities are underappreciated: While investors remain nervous about the outlook for commercial real estate, residential real estate is providing some potentially underappreciated opportunities. The coronavirus pandemic and its aftermath created distortions in many parts of the real estate market, most severely felt in the offices subsector, but in other areas also. In the residential space, for example, multifamily housing starts—properties that incorporate multiple residences within a single building or complex—ballooned to over 500,000 units in 2022,4 driven by a boom in demand. This is projected to slow considerably in 2025, as slowing rental growth, rising unemployment, and tightening commercial real estate financing conditions all impact the multifamily sector. But, while there are specific markets that will remain oversupplied, many parts of the U.S. continue to face significant shortages in residential housing, creating a supportive backdrop for potential rental growth for landlords. With this in mind, we are finding opportunities in select real estate investment trusts, while certain small‑ and mid‑cap building products companies also look appealing in areas where housing is constrained.

Energy productivity is a key challenge: Increasing energy productivity is crucial for the U.S. economy and a primary focus for executives across the energy complex. With cost curves for the exploration and production (E&P) of oil and gas rising, improving energy productivity is essential. Innovation and technology are pivotal elements of the solution, and many small‑ and mid‑cap energy companies are at the forefront of this innovation, often representing integral components along the energy supply chain. In particular, we see midstream operations—the processing, storing, and transportation of oil and gas—as being the biggest challenge for most major E&P companies and potentially a major opportunity for smaller companies that can provide these key services or enabling technologies.

The pronounced importance of active management

While there are good reasons to be optimistic about the smaller‑company outlook, it should be noted that ongoing challenges, such as stubborn inflation and higher interest rates, will continue to impact some companies more significantly than others. As such, we are likely to see increased dispersion among smaller company winners and losers moving forward. In this environment, we believe active managers with dedicated research capabilities and long‑term expertise in valuing smaller businesses, often in under researched or novel market areas, are best positioned to identify those winners, while at the same time, avoiding more of the potential losers.

U.S. smaller companies have been disproportionately impacted by the generally more risk‑averse sentiment that has prevailed in recent years. Relative valuations versus larger companies have fallen to historically low levels, despite earnings remaining broadly resilient. This suggests a disconnect between small‑cap prices and underlying fundamentals. Any signs of earnings improvement could provide the catalyst for smaller companies to be rerated higher. There certainly appear to be structural trends to support such an expectation. And history tells us that small‑caps have tended to outperform strongly coming out of a slowdown, and for an extended time. We believe that we may be on the cusp of this kind of smaller‑company outperformance cycle.

Risks—The following risks are materially relevant to the strategy

Small and mid‑cap risk—Small and mid‑size company stock prices can be more volatile than stock prices of larger companies.

General Risks

Equity risk—Equities can lose value rapidly for a variety of reasons and can remain at low prices indefinitely.

ESG and Sustainability risk—ESG and Sustainability risk may result in a material negative impact on the value of an investment and performance of the fund.

Geographic concentration risk—Geographic concentration risk may result in performance being more strongly affected by any social, political, economic, environmental or market conditions affecting those countries or regions in which the Fund’s assets are concentrated.

Investment fund risk—Investing in funds involves certain risks an investor would not face if investing in markets directly.

Management risk—Management risk may result in potential conflicts of interest relating to the obligations of the investment manager.

Market risk—Market risk may subject the fund to experience losses caused by unexpected changes in a wide variety of factors.

Operational risk—Operational risk may cause losses as a result.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.

July 2024 / INVESTMENT INSIGHTS

Matt Mahon is portfolio manager of the US Smaller Companies Equity Strategy at T. Rowe Price Investment Management. He is a vice president and member of the Small-Cap Stock and Mid-Cap Growth Investment Advisory Committees and a member of the Institutional Small-Cap Stock and Institutional Mid-Cap Equity Growth Investment Advisory Committees. Matt also is a vice president of T. Rowe Price Group, Inc.