2024年10月 / 觀點

U.S. Election: What's at stake for M&A and antitrust policy?

(僅提供英文版本) Next president to decide if tough antitrust policy continues.

Key Insights

- Joe Biden’s stepped-up effort to curb anticompetitive mergers and business practices was a departure from the past 45-plus years.

- Who the next president chooses to oversee antitrust enforcement will influence whether the agencies take an aggressive tack or opt to moderate their actions.

- Federal policy is only part of the puzzle. The outlooks for interest rates and the economy also play important roles in determining the level of M&A activity.

The Biden administration’s effort to crack down on unfair business practices marked a paradigm shift from the approach that generally had held sway for more than 45 years.

Will the Department of Justice (DoJ) and Federal Trade Commission (FTC) continue their assertive antitrust enforcement after the U.S. election?

This thorny question is important for markets. A string of abandoned mergers and acquisitions (M&A) and high-profile lawsuits for alleged anticompetitive behaviors have created uncertainty for the companies involved—and those companies that could find themselves in regulators’ sights.

Whoever becomes president—whether it’s Democrat Kamala Harris or Republican Donald Trump—has the potential to shape the focus and forcefulness of antitrust policy.

How Biden inaugurated a stricter approach to antitrust

Early in his presidency, Joe Biden issued an executive order calling on federal regulators to take a stronger approach to enforcing antitrust laws.

FTC Chair Lina Khan and DoJ Antitrust Division chief Jonathan Kanter have heeded this directive, seeking to curb what they view as excessive industry consolidation and to expand the grounds for antitrust action:

Not settling: Regulators have been disinclined to approve problematic M&A transactions by accepting concessions, such as divesting some parts of the acquired business. These settlements are viewed with skepticism.

New M&A rules: Revamped DoJ and FTC guidelines require much more detail about proposed transactions and flag deals that would boost the combined companies’ market share to more than 30%.

Testing the limits: Antitrust enforcement typically has been based on consumer welfare, which often focuses on the risk of unfair price increases. Recent lawsuits have sought to expand this standard, arguing, for example, that certain M&A transactions would harm workers and creators by reducing competition for labor.

Study hour: Regulators have used their authority to study and publicize areas of possible concern, including private equity’s forays into health care and issues that might arise in the technology stack for artificial intelligence.

On task: Antitrust enforcers have formed task forces with other agencies, including one focused on potential competition issues in the health care sector.

Stepped-up oversight has contributed to M&A weakness

So far, the percentage of M&A transactions that Biden’s regulators have flagged for potential antitrust issues has been in range with historical norms from past Democratic and Republican administrations.

Treatment of criticized deals, however, has changed. The number of abandoned M&A transactions has increased significantly.

Companies gave up on more than 20 proposed mergers because of competition concerns that the DoJ raised during Kanter’s first two and a half years heading the agency’s Antitrust Division.1

And the prospect of regulatory scrutiny appears to have been a deterrent, stemming the number of potentially problematic deals making it to regulators for review.

Party views on antitrust have blurred, but historical biases are likely to hold

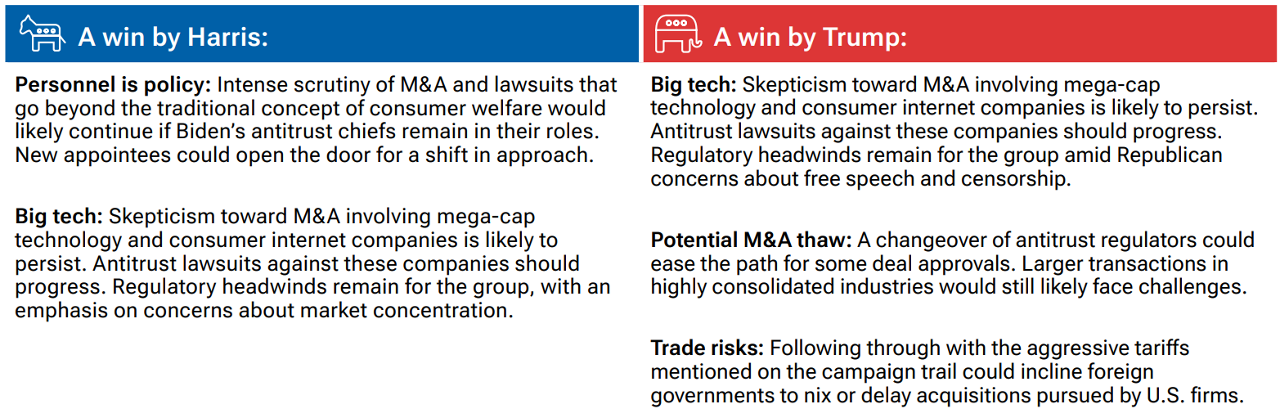

The Republican Party traditionally has taken a lighter touch when it comes to regulation.

However, the populist instincts of former President Trump and his running mate, Ohio Senator J.D. Vance, have raised questions about whether a win for their ticket would be as friendly to business interests as previous Republican administrations. The media has made much of Vance and other high-profile Republicans’ respect for FTC Chair Lina Khan’s efforts to challenge the dominant tech companies. These affinities could have their limits, given Trump’s stated penchant for deregulation.

That said, the FTC and the DoJ would likely focus on addressing anticompetitive practices in health care and concerns about the concentration power among the dominant consumer internet companies regardless of whether Trump or Harris is in the White House.

Less is known about Harris’s views on antitrust enforcement. However, her campaign’s emphasis on fighting to lower costs for families seems to align with the Biden administration’s antitrust initiatives.

Post-election developments will shape the outlook for M&A and antitrust

History tells us that enforcement of antitrust laws and challenges to large M&A will happen regardless of which party is in the White House.

However, who the next president chooses to helm the FTC and the DoJ’s Antitrust Division will influence whether the agencies take an aggressive tack or opt to moderate their actions. These personnel decisions bear watching.

At the same time, regulatory policy and federal oversight are only parts of the puzzle.

Some states have become increasingly proactive in seeking to restrict anticompetitive business practices. The judiciary also has a say. Decisions in antitrust cases that go to court are important in establishing legal precedents. And CEOs’ confidence in the outlook for interest rates and the economy plays a significant role in determining the level of M&A activity.

The U.S. election and antitrust oversight: What to watch

IMPORTANT INFORMATION

Where securities are mentioned, the specific securities identified and described are for informational purposes only and do not represent recommendations.

This material is being furnished for general informational purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. Investment involves risks. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

Gilad Fortgang is an associate analyst covering Washington and regulatory research in the T. Rowe Price Investment Management U.S. Equity Division.