July 2024 / INVESTMENT INSIGHTS

M&A revival means management quality matters even more

The M&A recovery creates opportunities, especially in mid-cap stocks

Key Insights

- Pent‑up demand and stabilizing economic conditions are driving a recovery in mergers and acquisitions (M&A) activity.

- Seeding a portfolio with companies that are potential takeover targets can add value. However, the timing of the harvest and the size of the deal premium are uncertain.

- The strength of a company’s management team can make a big difference in whether M&A creates value for the acquirer.

Mergers and acquisitions (M&A) activity has been heating up in the U.S. after an extended winter.

This thaw in dealmaking creates potential upside opportunities. Takeover bids typically come in above the target’s pre‑deal stock price, although the size of these premiums vary.

Risks also abound. Acquirers historically have struggled to add value through M&A, especially on larger deals.1

The M&A recovery gives well‑resourced portfolio managers a chance to add value for clients, especially in mid‑cap stocks.

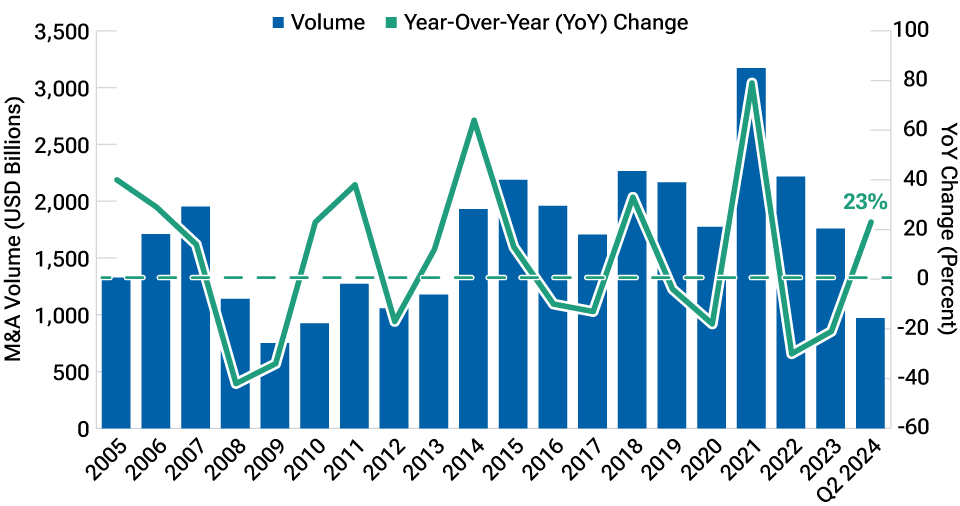

U.S. M&A volume is up 23% in 20241 after two consecutive down years

(Fig. 1) Annual M&A involving U.S. buyers and targets

Source: Bloomberg Finance L.P.

1 Announced, pending, and closed M&A transactions through June 30, 2024, were up 23% relative to the first 6 months of 2023.

Three factors fueling a U.S. M&A revival

- Pent‑up demand: M&A volumes had declined for two straight years at the end of 2023, as rapidly rising interest rates and uncertainty about the outlook for inflation and the economy weighed on business sentiment.

- Management fatigue: Navigating this challenging macroeconomic backdrop, along with disruptions stemming from the pandemic, took its toll on management teams. This weariness could make private and public companies more willing to sell.

- Improved economic backdrop: Management teams often shy away from pursuing acquisitions during periods of heightened uncertainty. The M&A recovery should have legs for as long as corporate management teams expect economic conditions to remain stable.

The appeal of takeover optionality

A portfolio seeded with stocks that eventually could be acquisition targets has the potential to enhance client returns over the long term. However, the timing of the harvest is uncertain, as is the size of the deal premium.

These considerations are front of mind when I’m weighing whether a company could find itself on someone’s takeout menu.

Business quality: An acceptable takeover bid may never materialize, so focusing on companies with strong business fundamentals and other sources of upside potential is critical.

Strategic value: The potential takeover target should offer an acquirer access to promising innovations or the prospect of stronger growth or profitability over time. The biotech industry, for example, is home to a profusion of smaller companies pursuing novel treatments. And larger pharmaceutical companies are willing buyers because they face pressure to replenish drug development pipelines as patents expire.

M&A a logical next step: Companies with promising products or technologies that eventually would benefit from being part of a larger sales organization may be willing fodder for acquisition. The same goes for founder‑led companies where the next leader is unclear.

Bottom line: An uptick in M&A could provide a tailwind for mid‑cap portfolio managers who favor high‑quality growth stories that might catch the eye of potential acquirers.

The other side of the deal

The environment for public companies interested in acquiring private assets strikes us as favorable.

On the supply side, private equity faces pressure to monetize existing investments after the lull in M&A and initial public offerings that occurred in recent years. Venture capital‑backed companies that could face challenges scaling their business and achieving profitability could also be more open to a sale.

In highly fragmented industries with many smaller players, like real estate or route‑based businesses such as pest control or food distribution, the efficiencies that come with being part of a larger organization can create value for an acquirer. Larger public companies in these industries may also have a higher valuation than the multiple paid to purchase a smaller operator, creating a potential arbitrage opportunity.

Management quality: A key leading indicator

The strength of a company’s management team can make a significant difference in whether an acquisition ends up creating value for shareholders over time.

Thoughtful leaders are more likely to pursue deals with attractive terms that don’t require heroic assumptions to earn a sufficient spread over the acquirer’s cost of capital.

Strong management teams may also be more adept at identifying strategic acquisitions that give the firm a potentially longer runway for growth through internal investment and/or additional tuck‑in M&A. Life science tools and industrials are two industries where we have seen strong management teams execute this playbook.

Operational prowess is critical to integrating the acquired company in a timely manner and positioning the combined firm to exceed growth and return expectations from the merger or acquisition.

Understanding a management team’s motivations and priorities provides insights into how they might think about deploying the company’s capital. It can also help us to gauge whether they are more or less likely to execute well on M&A and create value for shareholders.

I look for companies that hold themselves to a high and specific hurdle for potential returns on invested capital when they are contemplating M&A.

In addition, when a company announces an acquisition, it’s critical to evaluate whether the projections underpinning the deal are likely to bear fruit for the combined company. Unfortunately, there are many examples where M&A made companies bigger but did not necessarily make them better.

Actively navigating the M&A recovery

A large active manager may have a leg up in navigating a resurgence in M&A because it can support a global team of experienced research analysts to offer both breadth of coverage and depth of knowledge.

With the resources to pursue their curiosity and creativity, these experts should be well positioned to help identify promising companies that may also offer takeover optionality while seeking to limit the damage from potentially value‑destroying M&A.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

Dante Pearson is the associate portfolio manager for the US Structured Active Mid-Cap Growth Strategy in the U.S. Equity Division. He is an Investment Advisory Committee member of the US All-Cap Opportunities Equity, US Structured Active Mid-Cap Growth, Small-Cap Growth Equity, and US Real Estate Equity Strategies. He is a vice president of T. Rowe Price Group, Inc.