May 2024 / INVESTMENT INSIGHTS

The quality factor: Its impact, foundation, and evolution

Secular components have become an important part of quality investing

Key Insights

- Quality has been a powerful driver of returns, in part, given its relationship to the consistency and compounding of shareholder returns.

- An assessment of quality should center on financial analysis to help understand corporate health; financial productivity; and a company’s competitiveness, management execution, and shareholder returns.

- Quality is increasingly being influenced by a company’s exposure to secular change. Companies aligned with long‑term, sustainable growth trends appear to be economically more resilient and fundamentally of higher quality.

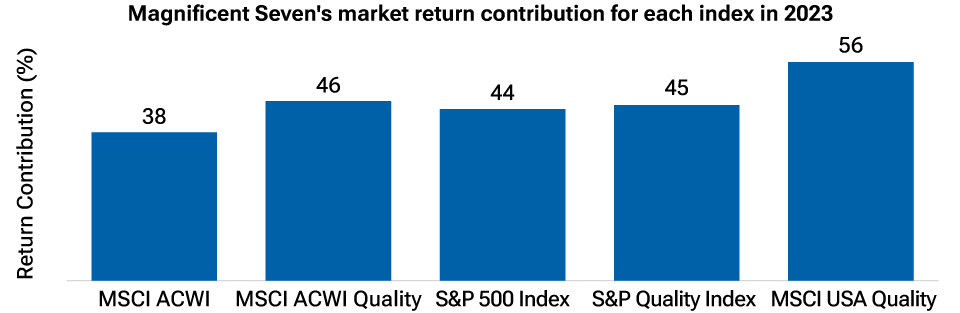

The investment landscape of the last 18 months has been unusual in many respects. Looking back, much of the rally has been driven by risk aversion easing back as black swan events were either avoided or diluted in probability. But while headline equity market returns might imply a robust economic backdrop, index returns were achieved despite an economic deceleration—but also because of a heavy concentration in a handful of stocks, most notably, the “Magnificent Seven”1 (Figure 1). While these stocks might be loosely bonded by the emerging theme of artificial intelligence (AI) and its infrastructure and future applications, the extreme return concentration over that period merits deeper consideration.

Magnificent Seven ride to the rescue

(Fig. 1) 2023 market returns were dominated by a handful of stocks

As of December 31, 2023.

Past performance is not a reliable indicator of future performance.

Source: Financial data and analytics provider FactSet. Copyright 2024 FactSet. All Rights Reserved.

The market capitalization of the Magnificent Seven stocks is one clear linkage, but a key thread when looking at equity returns over the past decade has been a collective improvement in the quality of these companies. This show of quality intertwined with the expectation of future growth and improvement, and stemming from the AI revolution, is at the heart of why these companies have dominated equity returns.

What is quality, and does it work?

Factor definitions—including size, momentum, volatility, growth, and value—have long been viewed with a high degree of consensus among practitioners and academic researchers. While there are variations in the precise metrics used for definition, many factor concepts are widely accepted and understood by investors.

Quality, either as a factor or as an investing style, is a notion that lacks a universally agreed‑upon definition, however. This makes quality harder to identify and capture, despite strong consensus and evidence that it has strong linkages to financial returns within equity markets.

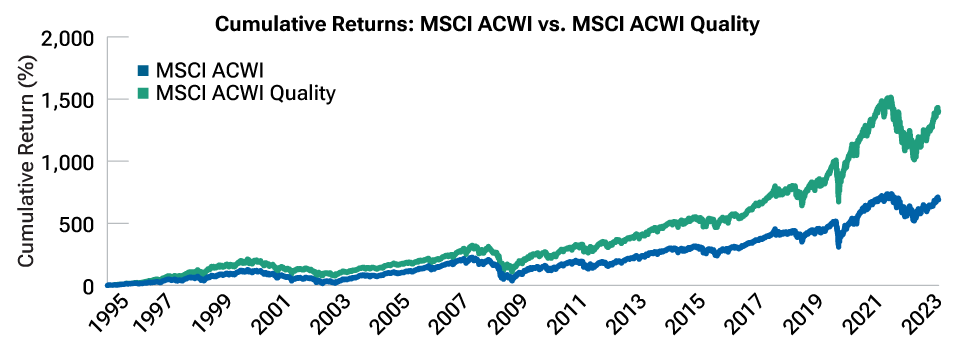

We examined quality from both a quantitative and qualitative perspective with a goal to understand its foundations, its impact on returns, and its redistribution in an ever‑increasing digital world. As a starting point to understand why quality is a much‑debated concept, we compared the MSCI ACWI2 with the MSCI ACWI Quality (Figure 2). While there are many definitions available, the MSCI ACWI Quality aims to capture the performance of quality‑growth stocks by identifying securities with high quality scores based on three main fundamental variables: high return on equity (ROE), earnings stability, and low financial leverage.3

Quality stocks have outperformed for over 10 years

(Fig. 2) The last few years have seen a clear differentiator in performance of quality assets

As of December 31, 2023.

Past performance is not a reliable indicator of future performance.

Sources: Financial data and analytics provider FactSet. Copyright 2024 FactSet. All Rights Reserved. The findings here are universe‑specific to MSCI ACWI and MSCI ACWI Quality.

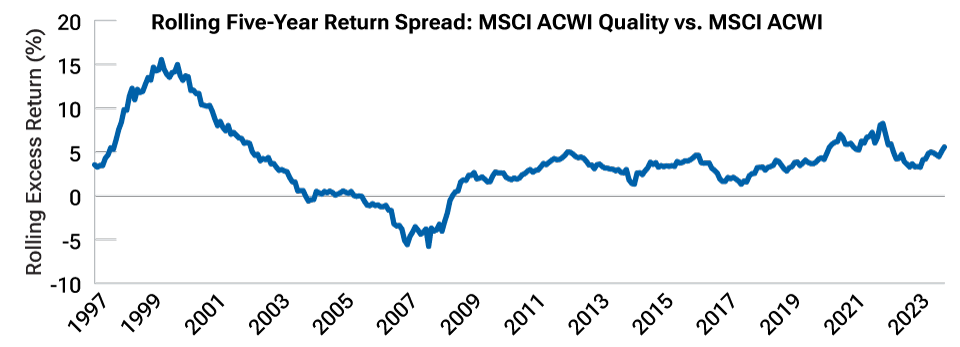

Outperformance of the quality index is notable, even more so when considering the five‑year rolling relative return of the quality index, which exceeds its mainstream equivalent in 85% of observations since 1997 (Figure 3). At least through the lens of one index definition, quality has been a consistent outperformer, albeit with cyclicality and notable periods of drawdown.

Long‑term outperformance of quality assets

(Fig. 3) Five‑year rolling relative returns of the quality index have exceeded its mainstream equivalent in 85% of observations since 1997

As of December 31, 2023.

Past performance is not a reliable indicator of future performance.

Source: Bloomberg Finance L.P. Monthly returns.

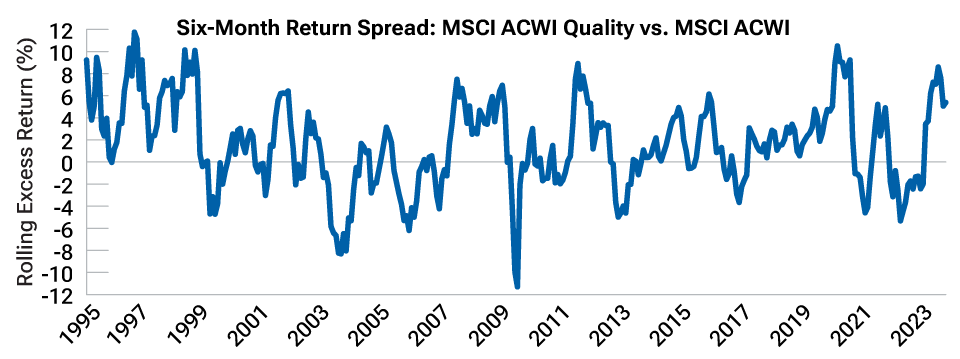

Risk attitudes define quality asset cycles

(Fig. 4) Quality often experiences underperformance during extreme risk‑on periods

As of December 31, 2023.

Past performance is not a reliable indicator of future performance.

Source: Bloomberg Finance L.P.

This cyclicality is better observed through an evaluation of shorter‑term data. In Figure 4, we show the same analysis over a rolling six‑month time frame, observing that the quality index often experienced underperformance during extreme risk‑on periods. These have often followed in the wake of crisis‑type events. This pattern is intuitive given that such recovery periods are often defined by broad‑based improvement and high‑risk tolerance. The exit from the financial crisis of 2008–2009 and the reopening of the global economy following the COVID‑19 pandemic are two such examples of quality underperformance.

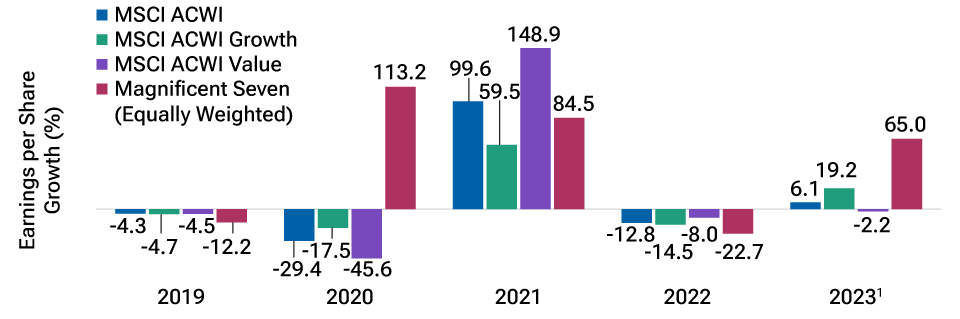

Robust reasons for outperformance of the Magnificent Seven

(Fig. 5) Since the pandemic, earnings growth has been markedly better than for other styles

As of December 31, 2023.

1 2023 consensus estimates. Actual outcomes may differ materially from estimates. Estimates are subject to change.

Sources: Financial data and analytics provider FactSet. Copyright 2024 FactSet. All Rights Reserved. T. Rowe Price.

With each observation representing six‑month periods rolled one month forward, we found that in 65% of observations, the MSCI ACWI Quality produced positive excess return relative to the MSCI ACWI. Midcycle and/or less directional markets are where quality tends to deliver a return advantage, especially where a scarcity component emerges. This growth scarcity was evident in 2023, and also in the period preceding the pandemic, where economic and earnings growth were muted. As with any scarce commodity, as growth becomes harder to come by, investors are more willing to pay a premium.

The more recent outperformance of quality has been driven by the absence of broad economic and earnings growth, in tandem with a concentration of earnings growth centered on the Magnificent Seven (Figure 5), a group of stocks that has risen in significance for quality investors.

Download the full article (PDF).

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

May 2024 / INVESTMENT INSIGHTS

Laurence Taylor is an equity solutions portfolio manager in the U.S. Equity Division. He is focused on creating custom solutions to match the sophisticated needs of our clients, leveraging our fundamental and integrated equity research and our tenured portfolio management capabilities. Laurence is a vice president of T. Rowe Price Group, Inc., and T. Rowe Price International Ltd.