April 2024 / INVESTMENT INSIGHTS

Are UK stocks too cheap to ignore

Improving fundamentals are not yet reflected in prices

Key Insights

- Despite an improving economic and political environment, UK equities are trading at what we regard as an excessive discount to U.S. and European stocks.

- Myriad factors could trigger a rerating of UK stocks: rate cuts, further positive economic data, a U.S. downturn, or new UK‑European Union (EU) trading arrangements.

- UK sectors that look particularly cheap relative to other markets include financials, health care, and materials.

Describing UK equities as “unloved” would be an understatement. At the end of March, they were trading at a near‑record discount to U.S. equities and at a major discount to other European equity markets. This is not particularly surprising given that money has been pouring out of UK stocks consistently since the Brexit vote in 2016. But with signs that the UK is returning to political and economic stability after a turbulent few years, could the negative sentiment toward the country’s stocks be about to turn?

The performance of the UK stock market is not just a matter of interest to those directly investing in it. At the end of March this year, the UK had a 14.5% weighting in the MSCI EAFE Index, second only to Japan at 23.7%. The UK’s weighting is well down from its post‑global financial crisis (GFC) peak of 23.1% in 2012 (Figure 1), but despite its current unpopularity, the UK equity market remains a large one in which many international firms are listed.

There is no denying that the recent decline in UK stock valuations is partly a function of relative weaker economic performance of the UK economy since the GFC. However, it is also partly down to Brexit: According to a report in February from the Office for Budget Responsibility, Britain’s decision to leave the EU has reduced gross domestic product (GDP) by 4% over the past eight years. The vote to leave the EU has caused major—albeit probably temporary—uncertainty over the UK’s trading and migration arrangements with the EU, and this has weighed heavily on FTSE valuations. However, it is likely that as the UK economy transitions to new trading relationships with the EU and other countries, this uncertainty will be significantly reduced.

The UK stock market remains a global player

(Fig. 1) Its weighting in the MSCI EAFE Index has fallen but remains significant

As of December 31, 2023.

Source: MSCI via FactSet (see Additional Disclosure).

Despite the looming election, political risk has subsided

There are reasons to believe the prospects for UK stocks are more positive than implied by current valuations. For one thing, the political turbulence of recent years has subsided. Regardless of who wins the next election, both political parties strongly support stable governance, fiscal responsibility, and the removal of regulations to boost growth.

The UK’s economy also looks in better shape and may outperform the eurozone in 2024. Real wages growth will support consumption in both the UK and eurozone because of real wage catch‑up in both areas. However, Germany’s fiscal consolidation may weigh on demand in the eurozone this year, making it difficult for firms to pass on higher wage costs to consumers. By contrast, tax cuts in the UK will likely boost consumer demand, enabling UK firms to pass through rises in real wage costs—meaning profits will not have to fall to the same degree.

Geopolitical risks could also lead to a renewed drive for economic and security integration between the EU and the UK. In a world of multiple ongoing conflicts, the contribution that the UK could make to Europe’s security will likely eventually lead the EU to agree to a much more favorable economic agreement with its former member, regardless of which party is in power in the UK.

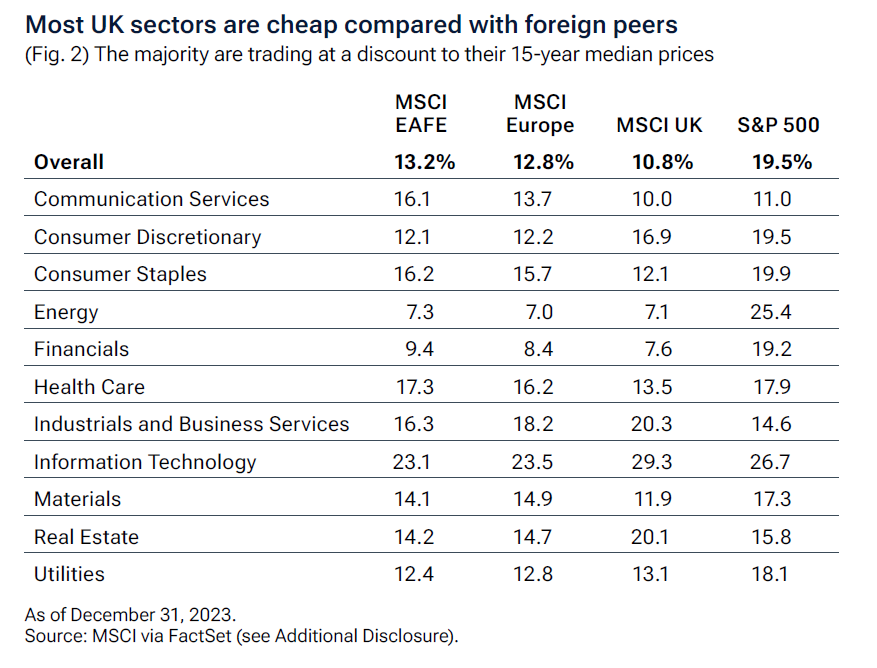

Most UK sectors look cheap compared with rivals

The improving political and economic picture has not yet been priced into valuations: Almost all UK industries are trading at a discount to their U.S. peers, and more than half are trading at a discount to their European peers (Figure 2). As of March 11, the FTSE 100 had a free cash flow yield of more than 6% and a price/earnings ratio below both its historic average and other indices. Most UK sectors are also trading at a discount to their 15‑year median prices, whereas most U.S. sectors are expensive relative to recent history. UK sectors that look particularly cheap relative to other markets include financials, health care, and materials. UK energy stocks are also trading at a discount to U.S. energy stocks, although they are priced at a similar level to European energy stocks.

One of the reasons the UK stock market has lagged the U.S. is that it is much less exposed to high‑growth mega‑cap tech companies, which have propelled the S&P 500 Index to record levels (Figure 3). The UK market’s large exposure to oils, banks, miners, and insurers has been far less attractive by comparison. Yet with valuations so low, there is an opportunity to pick up bargains in UK sectors that have the potential to rise sharply if sentiment improves.

The gap between U.S. valuations and other countries has widened dramatically

(Fig. 3) The S&P 500 has soared in value over the past decade

As of December 31, 2023.

Hopes of such an improvement increased in March this year, when official figures showed that UK GDP rose 0.2% in January—the first growth announcement since recession was declared in February. Further good news on the economy, rate cuts, and even a downturn in the U.S. could serve as catalysts to a rerating of UK stocks. As the UK moves beyond the political and economic uncertainty unleashed by Brexit and establishes new trading relationships with the EU and other countries, any positive developments such as these could have a major impact on UK stock prices.

Overall, we believe the UK continues to offer very good value compared with other markets. And, given the size and continued importance of the UK stock market relative to its non‑U.S. peers, this is something that international investors should pay close attention to.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

April 2024 / INVESTMENT INSIGHTS

Tomasz Wieladek is the chief European economist in the Fixed Income Division in London. Tomasz is a vice president of T. Rowe Price Group, Inc.

Federico Santilli is a portfolio manager covering international equity in the International Equity Division. He is an executive vice president of T. Rowe Price International Funds, Inc., and T. Rowe Price Institutional International Funds. He also is a vice president of T. Rowe Price Group, Inc., and T. Rowe Price International Ltd.