May 2024 / INVESTMENT INSIGHTS

Opportunities in fixed income for investors moving out of cash

Income and growth attributes can help investors put cash to work

Key insights

- With uncertainty around the path of cash rates, it is time for investors to consider stepping out of cash.

- We believe fixed income is an attractive place to redeploy cash, particularly for investors seeking to lock in income as bond yields are near historic highs.

- With diverse sectors, fixed income solutions can potentially help support investors with a range of goals and risk tolerances.

With the path of cash rates somewhat uncertain, we think it is time for investors to consider redeploying into the market. But where? With bond yields close to historic highs, we believe that fixed income is an attractive asset class to put cash to work—especially for investors seeking to lock in income.

Why we believe it’s time to step out of cash

Cash has been king these past few years. The combination of market uncertainty and high short‑term interest rates has resulted in a record amount of money held in money market funds. But staying parked in cash over a medium‑ and long‑term horizon could mean missing out on capital appreciation opportunities elsewhere. Furthermore, it’s not certain where cash rates go from here. On the one hand, its possible cash rates stay high, especially if labor markets remain tight. On the other, there is a case to be made for cash rates to fall, especially in Europe and select emerging markets, where there has been more progress in bringing down inflation.

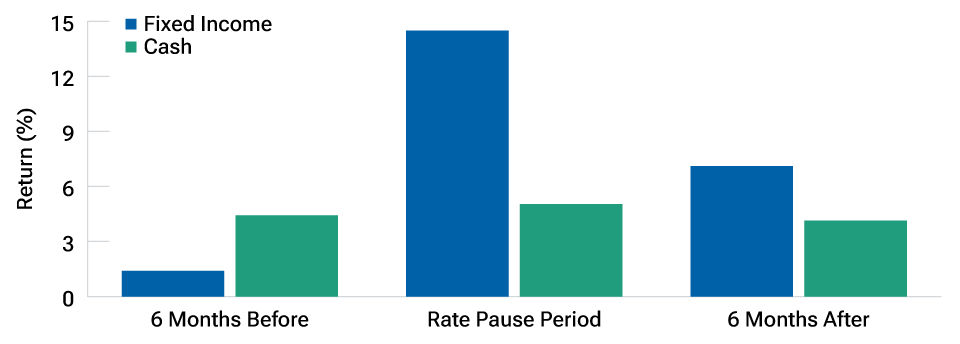

Against this backdrop, we believe it is a good time for investors to consider stepping out of cash and into the markets again. The current monetary policy pause may signal a good opportunity to do so—a review of past Federal Reserve policy cycles suggests it was typically beneficial for investors to deploy cash when rates peaked (see Fig. 1).

A rate pause signals opportunity

(Fig. 1) Bonds have tended to outperform cash during rate pause periods

As of April 30, 2024.

Past performance is not a reliable indicator of future performance. For illustrative purposes only. This is not representative of actual investments and does not reflect any fees and expenses associated with investing. Indexes cannot be invested in directly.

Cash is represented by the Bloomberg U.S. Treasury Bills 1–3 Month Index, and bonds is represented by the Bloomberg U.S. Aggregate Bond Index. Historical average performance in the 6 months leading up to the last Federal Reserve rate hike, the rate pause period (between the last rate hike and first cut), and the 6 months after the first cut. Dates used for the last rate hike of a cycle are: 02/01/1995, 03/25/1997, 05/16/2000, 06/29/2006, 12/19/2018. Dates used for the first rate cut are: 07/06/1995, 09/29/1998, 01/03/2001, 09/18/2007, 08/01/2019.

Source: Bloomberg Finance L.P. Data analysis by T. Rowe Price.

Why move into fixed income?

With bond yields in several sectors near multiyear highs right now, we believe fixed income is an attractive place to deploy cash. Fixed income has diverse sector options that support a range of goals and risk tolerances. It offers opportunities for both defense and capital appreciation. The fragmented nature of the asset class means that what drives one sector of the market is different than another, so there’s often a wide dispersion among sector returns. This provides flexibility to choose sectors that suit distinct needs—generating consistent income, capital appreciation, or defense against equity market volatility.

Fixed income and equity markets have tended to move in tandem in recent years. This understandably raises questions about whether bonds can still deliver the benefits of diversification seen historically. Correlations between the asset classes could continue to be volatile. However, if an extreme market event or significant downturn puts major selling pressure on risk assets such as equity, we expect high‑quality government and corporate bonds to be an effective diversifier. At a minimum, they should provide longer‑term investors with potential liquidity—therefore optionality—needed to make portfolio adjustments in times of stress.

Bond solutions for different market environments

Given the volatility and uncertainty in markets in recent years, investors may be feeling apprehensive about stepping out of cash. But regardless of how they expect the market environment to evolve, we believe that investors can find a solution in fixed income to mitigate risks and address their objectives. Below, we explore three economic scenarios and the bond strategies potentially conducive to each.

Scenario 1: Growth

Investment solution: High Income. A scenario of moderate economic growth is our base case scenario. Investors anticipating this should consider high yield strategies as the healthy macro environment will likely be credit supportive. The risk of a significant spread widening is less of a concern in this environment, which should allow for potential comfortable income accumulation. Current all‑in yields available in high yield are attractive, so it’s a good time to potentially lock in high income. As of the end of March 2024, the average yield in global high yield corporate bonds was around 7.63%, much higher than the average yield of 6.39% observed in the last 10 years.1

Bond solutions for a range of economic environments

(Fig. 2) Strategies conducive to a growth, deterioration, or stagflation scenario

As of April 30, 2024.

For illustrative purposes only. This is not to be construed to be investment advice or a recommendation to take any particular investment action.

Investments involve risks, including possible loss of principal. Diversification cannot assure a profit or protect against loss in a declining market.

Source: T. Rowe Price.

A higher‑quality global multi‑sector bond approach is another appealing option. It can offer attractive income potential and diversified return sources. These types of solutions provide exposure to a variety of sectors, including governments and securitized, investment‑grade, and high yield corporate bonds. The broad range of sectors offers the potential to diversify alpha sources and lower volatility.

Scenario 2: Deterioration

Investment solution: High quality. A deterioration scenario would involve a decline in economic activity and deceleration of inflation, leading to interest rate cuts. For investors worried about this scenario, investment solutions that are higher quality can be useful, such as developed government bonds where there’s typically better liquidity than other fixed income segments. Furthermore, the significant repricing of bond yields these past few years has led to improved valuations in government bonds with yields at some of their highest levels since the global financial crisis.

Investment‑grade corporate bond strategies also offer a potential combination of consistent income and high‑quality duration. For example, the average yield in European investment‑grade corporate bonds stood at around 3.66% at the end of March—which is well above the average level of 1.46% observed in the last decade.2

Scenario 3: Stagflation

Investment solution: Diversification. A stagflation scenario would involve inflation reaccelerating and economic growth slowing. This could lead to further interest rate rises and weakness in risk markets, such as equity. Such an environment can be challenging for investors. But a good way to navigate is through utilizing alternative and very active management strategies that can potentially benefit from higher volatility. In particular, investors should consider solutions that can generate income while seeking to minimize interest rate risk and mitigate against severe risk‑off events. These include flexible strategies, such as absolute return. These are typically benchmark agnostic and can cast a broader net, with the potential to invest in a wide range of geographies, sectors, and security types. However, strategies within this category can vary significantly. If an investor is seeking diversification, it’s important to choose an approach that has either low or negative correlation with key market indexes, such as the S&P 500.

Short duration and lower‑beta multi‑asset credit strategies can also work in this scenario. The latter offers the ability to find diverse alpha sources across the broad credit market. Approaches that actively manage credit beta and duration risk can help to navigate volatile environments.

The combination of election risks, the soft global growth environment, sticky inflation, and lingering geopolitical issues may be unsettling for some investors—keeping many parked in cash. But with bond yields near historic highs, it is time to consider redeploying those cash assets to potentially lock in income at these attractive levels. In today’s ever‑evolving landscape, fixed income offers a wide range of opportunities, including strategies for income, defense, or capital appreciation purposes. Choosing an approach that prioritizes quality active research is essential. This can give investors greater confidence about shifting their cash holdings to take potential advantage of the attractive all‑in yields that are available.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.

May 2024 / INVESTMENT INSIGHTS

Kenneth Orchard is head of International Fixed Income. He is portfolio manager for the Global Multi-Sector Bond and Diversified Income Bond Strategies and co-portfolio manager for the International Bond Strategy. Kenneth is a member of the Fixed Income Steering Committee, cochair of the fixed income Sector Strategy Advisory Group, and a member of the European and UK Asset Allocation Committees. He is a vice president of T. Rowe Price Group, Inc., and T. Rowe Price International Ltd.